This paper suggests that the war on inflation, deficits/debt, the welfare state, regulation, unemployment insurance, and labour unions are a response to capitalism’s profitability crisis and that globalization is part of this larger dynamic. After examining trade, foreign direct investment and financial flows the authors suggest that globalization is not by and large the way multinationals have responded to their profitability problem, but that globalization it is largely a myth that has been used to help reshape society in the interest of increasing the multinationals’ profitability. The World Trade organization can be seen as a having the purpose and potential to improve the profitability of the MNCs by lowering their taxes, their costs of production through its effects on labour and environmental legislation and by its ability to commodify much of what was out of the reach of the for-profit sector. Interestingly, decades of neoliberal rule does not seem to have restored the golden hue to capitalism. Market failure with respect to long-term investment and education are but two illustrations of why neo-liberal strategy, left to its own devices, my not be able to restore capital accumulation.

In the decade of the 1960s the world economy grew at the rate of 5.0 percent. In the 1970s the real growth rate dropped to 3.6 percent. By the 1980s the rate had dropped to 2.8 percent and continued this decline in the 1990s when it fell to 2.0 percent. In two decades capitalism lost 60 percent of its macroeconomic momentum (Thurow 1996: 1-2). Through the 1990s the overall European unemployment rate remained in double digits while the Japanese economy has been stagnating for a decade. The recent capitalist convert, Russia, appears to be demodernizing to Third World levels, while much of the Southern hemisphere has seen its social indicators deteriorating from already disastrous levels.

There is a significant body of evidence suggesting that capitalism entered into an economic crisis phase in the late 1960s due to a fall in the rate of profit as a consequence of the costs of production rising faster than productivity and/or price (Brenner 1998, Cherry 1987). Crisis in this context does not mean catastrophic economic breakdown or the end to capitalist social relations. Nor does it mean capitalism as usual (since 1945). The difference between capitalism’s business cycles and an economic crisis is that with non-crisis cyclical conditions, normal economic activity, within the context of prevailing social relationships, is sufficient to restore prosperity (Gordon 1980). By contrast crises undermine the stability of the institutional framework, because as accumulation slackens, less profit is available for the maintenance of those institutions whose relative stability and reproducibility permit the repeated fulfilment of an important socio-economic function.

Capitalism runs on profit. Without adequate profits, firms cannot invest in order to lower their costs of production, (e.g. robots) promote research and design in order to invent new products, produce new plants and equipment to meet increases in demand or to generate dividends for their owners. Non-competitive firms will not be able to stay in business because they will not be able to invest, pay their debts or advertise. Those firms with higher profits are better able to lower their costs of production, invent new products, and advertise to tell about their “successes” in production. Investments that generate less profits because costs (raw materials, machines and/or labor) are rising faster than productivity and/or price diminish the capacity and incentive to invest again. If this situation becomes the average condition for firms in an economy, stagnation or depression is the expected result.

It is the rate of profit that provides the capitalist class with the product to invest as well as the motive. As the rate of profit falls there is a tendency for investment, productivity, economic growth and tax revenue to follow while unemployment rises.

By standard accounting methods between 1965 and 1973 the rate of profit in the US in manufacturing and private business sectors fell by 40.9 percent and 29.3 percent respectively. The profitability decline in the US economy did not bottom out until the early 1980s (Brenner 1998: 95).

The rate of profit declined in the other major capitalist economies as well (Brenner 1998, Cherry 1987), albeit not necessarily on the same precise schedule, resulting in global stagnation and the creation of a crisis far more serious and enduring than a normal cyclical downturn. As a result capitalism has been suffering from a quarter century of economic slowdown. Stagnation has been the manifestation of this crisis in all of the advanced capitalist countries. While the crisis came earlier for some countries than others the profitability crisis is a global capitalist phenomena. The US is the country that appears to be the first to emerge from the crisis. As late as the period 1989-1997 the US economy grew an average of 2.3% a year, less than Germany’s (2.6%) and Japan’s (2.4%). Even the 1994-1997 period US growth of 3.0% was not significantly higher than Europe’s 2.4% (Left Business Observer 1998: 3). It is in only in 1997 that the US has emerged with signs of a more vital macroeconomy. The question becomes how has capitalism managed its profitability crisis?

In the face of falling profits corporations are compelled to find means of reducing their costs by lowering their wages and taxes and/or raising their productivity. Some of these methods represent advanced capitalism’s “intensive” method of reducing costs through increases in productivity by means of mechanization. However, other methods of responding to the profitability crises have included “a return to extensive methods,” including longer hours, lower wages, and deteriorating low cost working and environmental conditions. A generation of high national and international levels of unemployment and “globalization” have made labour more vulnerable. The real and threatened effects of unemployment and globalization (capital flight) tend to lower worker’s expectations with respect to wages, benefits and working conditions as well as citizens’ expectations with respect to health, education and welfare.

During this period of crisis the conditions of economic stagnation have given rise to a corresponding political response. The real or increased threat of “capital flight” due to competitive pressures and enhanced by the growing technological possibilities to do so, imposed on governments “the need” to introduce attacks on labour in general and state salaried employees in particular. Attacks on the welfare state (in the form of the war on deficits and debts), wages, unions and government in general are, along with the socialization of private debt are arguably attempts by capital to restore profitability by using its increased influence over the state in its own interest.

Why then is declining investment (capital strike), unemployment, increasing poverty, falling wages, a shortage of tax revenue, an attack on the welfare state, and qualitative social and institutional change part of this process of restoring profitability? For capital the resolution to the crisis requires means of restoring profitability. A number of strategies have been employed to this end over the past quarter century.

Contemporary economic orthodoxy has failed to establish that inflation rates up to 8% have any negative impact on the economy or that zero inflation maximizes economic growth (Sarel 1996). And yet the US central bank and many other central banks have made the attack on inflation its prime goal over the past few decades. The war on inflation is accomplished by restricting the availability of money and credit and therefore keeping interest rates high, discouraging investment and making it more difficult for the low profit firms with their relatively inefficient capital to stay in business.

The alternative explanation for this strategy is that the underlying goal is to lower wages and resistance to labor intensity by increasing unemployment and lowering workers’ expectations. This helps industry while preserving the value of the debt and therefore the source of profits of the financial industry.

Tax cuts for the corporate sector and the wealthy helps to redistribute income upwards.

The threat of and direct foreign investment in non-unionized countries and in areas of developed countries where wages, taxes and environmental regulations tend to favour business lowers costs and raises profits.

Reducing government imposed regulations tends to lower prices of the affected industry and wages of its workers. The institutional transformation that takes place is that the firms themselves re-regulate the industries so that they may better determine wages and benefits.

The weeding out of all but the most productive and profitable means of production results in less capital available as well as layoffs, wage reductions, benefits cuts and speedups at work. The same profitability crisis that led to the downsizing process and the merger movement resulted in a massive number of bankruptcies and a destruction of capital not seen since the Great Depression. The general effect of this is that only the more efficient and profitable capital is left standing.

A strategic obsession with government deficits and debt, the corresponding attack on the welfare state and the lowering of the taxes of the corporations increases the insecurity and dependency of everybody else. The emphasis on the market, minimalist state and individual/family responsibility are all soldiers in the war against the welfare state reflected in declining state expenditures and the privatization of the public sector.

It would be hard to exaggerate the degree to which the concept of globalization has penetrated our culture. It is treated at once as an economic tidal wave and a paralyzer of the state. It has been used to justify deregulation, privatization, environmental degradation, free trade, deficit/debt mania, high interest rates, zero inflation targets, anti-labour legislation, cuts to social spending and upper income and corporate taxes. These policies are of course executed by individual nation states. The rationale in defence of these policy changes is that the rules established by the now dominant transnational corporations and the uncontrollable high speed market highway they travel on must be obeyed lest you be run over and/or left behind. The trouble with the concept of globalization is that objectively it is largely a myth, while the consequences of its power to organize our thoughts as to how the world works has real effects.

Weiss (1997) identifies a spectrum of hypotheses with respect to globalization ranging from strong to weak. The strong globalization hypothesis views the rapid growth of economic interdependence as a reflection of an emerging supra-national phenomenon which is distinct from the three decades following the Second World War when the expansion of world trade and finance was primarily led by the concerted efforts of nation states through the creation of an international financial system (Bretton Woods) and successive rounds of multilateral tariff reductions under GATT (General Agreement on Tariffs and Trade). According to this view, the era of internationalism has run it course, and has given way to a new phase of international political economy—a new “globalism” or “borderless” economy, in which the internationalization of production is identified as the driving mechanism of economic integration. In such a ‘borderless’ world it is claimed that footloose transnational corporations (TNCs), rather than nation states, are spearheading “global” economic interdependence eroding the national differences and making domestic strategies of national economic management increasingly irrelevant (Ohmae 1990, Reich 1992, Horsman and Marshall 1994, Hamdani 1997). In this view, TNCs are claimed to be the dominant economic entities. These truly global TNCs own and control subsidiaries, engage in business alliances and networks in different locations of the “borderless” world, source their inputs of labor, capital, raw materials and intermediate products from whenever it is the best to do so, and sell their goods and services in each of the main markets of the world (Dunning 1997). Globalization is therefore, according to this view, “triggering a process of systematic convergence in which all governments face pressures to pursue more or less similar policies to enhance their national (or regional) competitiveness, vis-à-vis other countries, as locations for international production” (Hamdani 1997: 3).

The erosion of state power is however, contested by a second hypothesis of globalization, which holds that states never had total macroeconomic planning power before the emergence of globalization. However, those powers that it had and continues to have are significant (The Economist 1995).

In contrast to the strong hypotheses of globalization, the weak hypotheses view the rapid expansion of cross-border trade, investment and technological transfer, and the greater integration of national economies not so much as a reflection of a globalized world, but rather as a more internationalized world where national and regional differences, including national institutions, remain substantial (Chang 1998, Dymski and Isenberg 1998, Hirst and Thompson 1996, Weiss 1997). From this perspective the external and internal constraints that strong internationalization tendencies impose on the nation states are viewed to be relative rather than absolute, and they represent an evolving history of state adaptation to both external and internal challenges rather than ‘the end of state history’. According to this view, many of the recent difficulties national policy makers have experienced with macroeconomic management, such as balancing budgets, have more to do with internal fiscal difficulties caused by the years of slow economic growth, prolonged recessions and demographic changes, than with the ‘globalization’ tendencies.

To assess the extent and patterns of globalization and its limits and counter-tendencies, we follow the commonly used quantitative approach with it focus on trade flows of goods and services, and capital flows (Hirst and Thompson 1996, Weiss 1997).

All interpretations of globalization recognize the sheer volume of cross-border flows of capital, goods and services and the growing interdependence and integration among the main world markets. However, the central issues in the debate are three: (i) Do these trade and investment flows indicate an historically unprecedented trend; (ii) How substantive are these flows compared to their corresponding flows in earlier periods; and (iii) To what extent are these flows world-wide in scope.

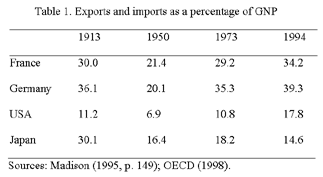

In their historical comparison of the international economy and its regimes of regulation during the Gold Standard period (1870-1914) with the international economy during the 1980s and early 1990s, Hirst and Thompson (1996) look at a wide range of measures of integration, including the share of merchandise trade (export and imports) in output (gross national product, GNP). Their results indicate that our highly internationalized economy is not unprecedented. In some respects the current international economy is less open than the system that prevailed during the Gold Standard period (1870-1914). Table 1 indicates the extent of internationalization, as measured by the sum of exports plus imports as a percentage of GNP of a number of advanced industrialized countries. In 1973, the share of exports and imports in GNP in most industrialized countries was lower than in 1913.

The degree of integration into the world economy was even more limited for most regions of the developing world, with the exception of East Asia. For the developing countries as a whole the share of exports plus imports in GNP rose from an average annual rate 28 percent during the 1960s to 34.4 percent in the 1970s and 38.4 percent in the 1980s (Hirst and Thompson 1996: 28).

The only region of the developing world that underwent a great deal of internationalization was East Asia, where the share exports plus imports in GNP rose from 47 percent in the 1960s to 69.5 percent in the 1970s and 87.2 percent in the 1980s. Africa’s share of exports plus imports in GNP actually dropped slightly between the 1970s and 1980, as did the Middle East where the downturn in oil prices reduced the region’s share of exports and imports in GNP. The marginalization of most of the low wage regions of the developing countries from the ‘globalized’ world economy becomes more evident if one focuses on the geographic distribution of trade and investment flows.

In order to assess the extent to which the recent increases in trade flows have been global in scope, it is necessary to examine trade flows by region of origin and destination. Table 2 indicates that trade flows are highly concentrated among the rich OECD countries in general and within the three large regional trading blocks of the European Union, North American and Japan in particular. In 1996, exports and imports by the OECD countries accounted for three quarters of total world exports and imports. The European Union (EU) as a trading block does not appear to be more integrated into the world economy. Intra-EU exports and imports have continued to account for almost 62 percent of the total of EU exports and imports. The growing importance of intra-EU trade indicates a clear trend towards “Europeanization” rather than toward “globalization” as suggested by globalization theorists.

The growing importance of Japan’s trade flows with the dynamic Asian economies also indicates a trend towards “Asianization” rather than ‘globalization’. As Table 2 indicates Japanese exports to the dynamic Asian economies more than doubled over the period 1972-1996, thus reversing the traditional dominance of trade with the United States.

There are various measures of capital mobility. According to one broad definition, net capital mobility is measured as the absolute value of current account divided by GDP (gross domestic product). According to this measure of capital mobility, today net capital flows are huge in terms of their absolute size, but they are not historically unprecedented. The peak, peace-time years for net capital flows for the 11 OECD and Argentina were 1870-1889 followed by 1890-1913, when international capital flows topped 3.7 and 3.2 percent of GDP, respectively (Obstfeld 1998: Table 1). The corresponding ratio for the period 1990-1996 was 2.3 percent. Two other measurements of capital mobility are foreign direct investment and cross-border trade in bonds and equities.

If trends in trade cannot be used to support globalization theory then it might be suggested that this is to be expected. After all in a truly globalized economy direct foreign investment might be expected to replace exports, as capital, free to move where it wants, will locate in low wage, low tax countries.

One of the important structural changes in the world economy during the post war period has been the shift in the relative importance of trade and FDI (foreign direct investment). The relative importance of trade in the world economy has been declining since the early 1980s. The total accumulated (inward) stock of FDI grew at an average annual rate of 18.2 percent during the period 1986-1990 and 9.7 percent during the period 1991-95 (United Nations 1998: 2). Over the same period the total nominal value of exports of goods and services grew at an average annual rate of 14.6 and 8.9 percent, respectively (United Nations 1998: 2).

This rapid growth in FDI is often taken by the globalization theorists as proxies for the ‘globalization’ of production in general and the dominance of MNCs (multinational corporations) in manufacturing production in particular. Instead of exporting goods, MNCs are serving foreign markets by building factories. However, a careful analysis of the aggregate FDI figures reveals the inappropriateness of these proxies, and thus the misleading conclusions drawn from these aggregate figures (Weiss 1997: 9).

Not all FDI flows are normally directed towards the establishment of new investment in manufacturing and other productive sectors of the economy of the host country. ‘Non productive’/speculative ventures, such as real estate, and the cross-border merger and acquisition activity of MNCs are estimated to account for a major portion of the aggregate FDI flows (Weiss 1997: 8-9). Cross-border merger and acquisition activity alone accounted for over half of FDI flows in the second half of the 1980s, and as much as 58 percent of FDI flows in 1997 (United Nations 1998: 19). Merger and acquisition activity expanded dramatically in the United States in the 1980s and 1990s. In 1997, merger and acquisition by foreign MNCs accounted for some 90 percent of FDI flows into the United States (United Nation 1998: 13). The corresponding ratios for the first and second half of the 1980s were 67 and 80 percent, respectively (Hirst and Thompson 1996: 71).

The significance of cross-border mergers and acquisitions is that what is taking place is simply a transfer of ownership, as MNCs attempt to consolidate their positions within the three trading blocks.

The available evidence also indicates a redistribution of the stock of outward FDI from primary and secondary towards the tertiary sector (services) over the period 1975-1990 (United Nations 1992: 18). Because it is not possible to internationally trade many services, MNCs must invest abroad to provide these location specific services. With the growing importance of services in the high-wage economies, investments in services by MNCs are expected to grow in the future.

To judge the significance of the internationalization of production and its recent trends, it may be useful to look at the trend of inward and outward FDI flows relative to the total investment in building, plants, machinery and equipment (fixed capital formation). If the strong globalization hypothesis holds, the data should show a large and increasing share of FDI in total investment. Taking the aggregate FDI figures at their face value, table 3 indicates that this is clearly not the case. FDI accounted for a small share of investment in both developed and developing countries and there is little indication that these shares are rising.

Like trade flows, investment flows are also almost exclusively concentrated in the advanced industrial states and a small number of rapidly developing industrial economies. In the beginning of the 1990s, 75 percent of the total accumulated stock was located in three trading blocks of North America, the European Union and Japan (Hirst and Thompson 1996: 63), a proportion which has not changed much since the end of 1970s (Brandt commission 1980). The triad, consisting of the European Union, Japan and the United States, also received approximately 70 of the world-wide FDI inflows in 1990, a proportion unchanged from the average of the decade of the 1980s (United Nations 1992: 20). The dynamic Asian economies accounted for over 60 percent of investment in the developing countries by MNCs. The concentration dropped moderately in the early 1990s as the major economies experienced a recession (United Nations 1998: 5).

This geographic distribution of investment by the MNCs is clearly in conflict with the strong globalization hypothesis, according to which a growing portion of investment by the MNCs should be world-wide in scope, and the low-wage and low tax developing economies should attract an increasing share of investment by footloose MNCs.

Several explanations are provided in the literature for the concentration of the MNCs activity, especially core technological activity, such as research and development, in the high-wage and high tax home countries. First, concentration in the same country/region provides a pooled market for knowledge-intensive labor, which tends to be treated increasingly as a fixed cost. With new technologies placing a premium on fixed costs, including machinery, equipment and specialized skills, the importance of raw material, wages and other variable costs is reduced. Second, the concentration allows for a close link between producers and specialized suppliers of inputs, especially in non-assembly operations. Third, home location provides the MNCs with a national institutional support system, including relationships with trade associations, training institutions, and more importantly local and national governments. The latter supporting relationship is of particular importance because “(b)eing generally exclusive rather than open to all, support relationships of this kind constitute a competitive advantage” (Weiss 1997: 10).

In Hirst and Thompson’s (1996: 96) examination of the home bias of the US, Japanese, German and the British manufacturing MNCs, the parent operations accounted for between 62 and 97 percent of total assets, and between 65 and 75 percent of total sales in 1992-1993. Similar findings are reported by Tyson (1991). The US manufacturing parent operations accounted for 78 percent of total assets, 70 percent of total sales, and 70 percent of total employment in 1988.

In the case of money and capital markets, the progressive internationalization of money and capital markets has been even more impressive, especially since the collapse of Bretton Woods in the early 1970s, and subsequent liberalization of exchange and capital controls (see table 4). The daily turnover on the world’s major exchange markets rose four fold between 1986 and 1993, reaching $1.0 trillion, or about 250 billion a year (IMF 1993: 24), i.e, 33 times the total value of world trade.

The progressive internationalization of money and capital is a marked change from the post war period. Whether this progressive internationalization of money and capital markets signifies a radical change indicating a globalized financial market or a tendency toward a globalized market, is not, however, clear, for at least two reasons. First, to assess whether the explosion in the cross-border financial flows represents a new phase in the international economy or simply a greater internationalization of finance we need to have some relatively clear model of what a truly global financial market would look like. Dymski and Isenberg (1998: 221) provide such as a rigorous model:

A financial market is internationalized when assets with idiosyncratic risk/return characteristics—that is, whose risks and returns are unique to the regulatory and banking structure of the country of origin—are sold offshore as well as domestically. A financial market is considered to be truly globalized when “it involves the continuous exchange in financial centers around the world of assets whose risk/return characteristics are independent of national regulatory and banking structures.... Globalization is, in effect, the end point of a process of the separation of financial asset characteristics (including prices) from the idiosyncrasies of their countries of origin.

Despite the explosion in cross-border financial flows during the recent years, the penetration of foreign assets into domestic financial markets is still relatively light and confined within the three trading blocks (Hirst and Thompson 1996: 40-44). The available evidence also suggests that the “home asset bias”—a tendency to invest in local assets—is strong even in financial markets. The available evidence on “home asset bias” in the equity portfolio of investors from several large industrial economies is quite revealing. The investors in the United States were more among the least diversified with the percentage of equity portfolio held in domestic equities equal to 98 percent in 1987, followed by Japan (87%), the United Kingdom (78%), Germany (75%) and France (64%) (Cooper and Kaplanis 1994). Moreover, whether the internationalizing financial markets will lead to a globalizing financial market remains in dispute (Boyer 1996, Wade, 1996).

Second, to the extent that the recent phenomenal growth of international financial flows and liquidity were brought about by policy specific and conjunctural factors, such as the international recession and the growth in government debt through the 1990s, the emergence of structural imbalances in payments for a number of large economies, and the liberalization and deregulation of financial markets by national governments and the abandonment of capital controls, these changes may be temporary (Hirst and Thompson 1996). The classical gold standard years 1889-1914 are also marked as a period with the lowest interest rate parity between the two world financial centres, New York and London, as measured by the standard deviation of the difference between one-year interest rates on sterling-denominated assets sold in New York and those sold in London (Obstfeld 1998: Figure 1). The progressive internationalization of money and capital markets acts as a double-edged sword. To the extent that cross-border financial flows spread risk across assets of various nationalities and redistribute savings across nations, such flows may enhance efficiency and capital accumulation. However, greater internationalization of financial markets also broadens the scope for financial speculation and redistribution of income, wealth, and political power toward a growing worldwide rentier class. As the most recent Asian and Mexican crises indicate, the internationalization of casino capitalism’ makes not only national economies more vulnerable to short-term capital and money movements, but it also contributes to greater interest rate and exchange rate volatility (Felix 1998). As Keynes (1967: 159) reminded us in 1936: “Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

What would capitalism like to do to increase its profitability? - World Trade Organization in context

In the first section of the paper we gave an account of the changes that took place within the nation state as a response to capitalism’s profitability crisis, which in part was justified as made necessary by the forces of globalization. In the second section of this paper it was established that the growth in real productive FDI was greatly exaggerated, which suggests that globalization is not by and large the way multinationals have responded to their profitability problem. If globalization is not a fact but rather largely a myth that has been used effectively to reshape society in the interest of increasing capital accumulation, the question becomes what next? Another example of how national governments make international rules and use these rules to overcome domestic resistance to the multinational’s interests is the World Trade Organization (WTO).

In 1995 the World Trade Organization (WTO) replaced the GATT. WTO rules have been described as international bill of rights for corporations. Trade negotiations are conducted by trade ministers, where MNCs’ economic interests are pursued to the exclusion of all else. When the Mulroney government in Canada was asked if any environmental assessment had been carried out on the impending free trade agreement between the U.S. and Canada, it responded that the trade deal was a commercial agreement and that the subject of the environment had not come up once—this is in an agreement that dealt with energy, agriculture, environmental standards, forests and fisheries (Shrybman 1999: 5).

The WTO agreement is an extensive list of policies, laws, and regulations that governments can no longer establish or maintain (Shrybman 1999: 6).

The WTO has extended the reach of trade rules into every sphere of economic, social and cultural activity. Historically, trade agreements were concerned with the international trade of goods such as manufactured products and commodities. The WTO, however, extended the ambit of international trade agreements to include investment measures, intellectual property rights, domestic regulations of all kinds, and services - areas of government policy and law that have very little, if anything, to do with trade, per se. It is now difficult to identify as an issue of social, cultural, economic or environmental significance that would not be covered by these new rules of “trade” (Shrybman 1999: 4)

Trade related investment measures is an example of one of many agreements that are on the agenda that would open all sections of a nation’s economy to foreign investment; to prevent governments from favoring domestic corporations; to establish the pre-eminence of corporate rights; and to enable foreign investors to enforce their new rights directly. The WTO agreement on trade in services in the area of health and education would effectively undermine the mechanisms with which publicly funded commitments exist to health care and education. Such an agreement would require governments to provide the same subsidies and funding support to private hospitals and schools as it makes them available to non-profit institutions in the public sector (Shrybman 1999: 16).

These rules of course apply to any government or community that attempts to infringe on MNCs “rights”. “Here are some examples of typical US state laws or legal principles that conflict with the WTO: laws that promote investment in recycled material markets; that allocate public deposits or banking business based on community reinvestment performance or local presence; that impose “buy local” requirements of preferences for state procurement; and that make state procurement contingent on certain social or human rights considerations, like the Macbride principles and Burma-selective purchase laws. Ninety-five laws have been identified as potentially “WTO-illegal” in California alone, according to the Georgetown University Law Center. How do we know this? Japan, the European Union and Canada publish documents every year that list American laws they consider WTO illegal” (Borosage 1999: 21).

WTO authority and influence stems from its powerful enforcement tools that ensure that all governments respect the new limits it places on their authority-trade sanctions that can cost hundreds of millions of dollars. While previous trade agreements allowed for similar sanctions, they could only be imposed with the consent of all GATT members, including the offending country. Now WTO rulings are automatically implemented unless blocked by a consensus of WTO members (Shrybman 1999).

The World Trade organization has a great deal of potential to improve the profitability of the MNCs by lowering their taxes, their costs of production through its effects on labour and environmental legislation and by its ability to commodify much of what was out of the reach of the for-profit sector.

“Footloose capital is free riding on less mobile taxpayers, getting the benefit of services provided by governments in high-taxing countries while paying taxes in low-tax jurisdictions, if at all.—Some EU governments also argue that tax competition makes it ever harder to tax mobile factors of production such as capital. Instead, they complain, they have to increase taxes on less mobile factors, notably labor, which may drive jobs away” (The Economist 2000: 9). Footloose capital of course need not move to the third world, but in the EU’s case simply from France to Ireland, even after Ireland’s growth has been subsidized by the EU.

While the World Trade Organization did not invent these “opportunities” it tends to make them more possible. So-called globalization cannot explain the ability of MNCs to extort low taxes from the state or to privatise the health or education sectors. These are political acts reflecting the relative power of capital at this juncture in our history. As Weiss (1999: 31) notes, “while the external world of capital flows exerts real constraints on how governments can behave, so too does the internal world of regime orientations, institutions, and domestic politics. Failure to understand the power of path dependency and the pull of domestic pressures leads many globalists systematically to overstate both the power of globalization to determine domestic outcomes and its casual importance in constraining policy choice.” One important implication of this perspective is that the most important limitations on the scope of state involvement in the economy and what it can ‘responsibly’ do to enhance productivity-enhancing growth and provide social protection may be self-imposed rather than externally induced. This is no more clear than in the United State where the two decades long self-imposed neoliberalism, has already exposed the acute contradictions of neoliberlism and its application to areas known for their spill-over effects and market failures, such as research and development activities as well as education and training.

The President�s Information Technology Advisory Committee (PITAC 1999) asks the question should we expect information technology research to be funded primarily by commercial interests? Their answer is no. The report argues that in the US essential long-term high-risk investments in the information technology (IT) sector are being sacrificed in part because of near term market pressures. This committee, made up of IT corporate executives and academics in related fields, goes on to explain that it is the federal government since WW2 that has provided the funding for IT research and has “trained most of our IT researchers” (PITAC 1999: 8). The effect of this is to have “seeded high risk research and yielded an impressive list of billion dollar IT industries � “ (PITAC 1999: 8). In both the public and private sectors today, US investments in technology R&D the committee argues have slowed to a relative trickle. American Businesses, in an ever shrinking and more highly competitive world, have devoted less and less of their precious resources to long term R&D, directing their efforts instead to reducing costs and getting new products into the pipeline today at the expense of the future. The federal government has mirrored this trend because of dramatically increasing pressures on research and development budgets, with only modest increase in funding levels.

Lester Thurow (1999) has identified the necessity of recognizing capitalism’s tendency for market failure with respect to long-term investment. He points out that private rates of return for R&D investments are on average less than half than the social rates of return accruing to society as a whole. There is powerful evidence that there are huge positive spillovers from research and development but that left to themselves firms will spend too little because they cannot capture all the benefits that flow from these investments. In addition to the more obvious disadvantages of self-interest in a competitive economy there is also the issue of the time frame that often dominates the competitive firm’s decision making. The private sector with its preoccupation with shareholders’ rates of return and competition operates on a short-run time frame and therefore tends not to invest in advancing basic knowledge. Very few companies are able to invest for a payoff that is years away. “The only private labs that have ever focused on anything other than short-run results are those such as Bell Labs and the IBM labs that were run by quasi-monopolies. The minute AT&T (forced by government) and IBM (forced by the market) joined the normal competitive capitalistic world, they cut long-term research out of their laboratory budgets “ (Thurow 1999: 291). In both the IT sector and biotechnology it is the state that has made all the high risk investment and then turned over the results to the private sector. “Moreover, many advances are broad in their applicability and complex enough to take several engineering iterations to get right, and so the key insights become public and a single company cannot recoup the research investment” (PITAC 1999: 79). Because governments are more likely to be indifferent to who reaps the benefits from investments in R&D and they have a general interest in creating an environment which is conducive to capital accumulation, the state plays an essential role with respect to long-term investment in capitalist economies.

What is true for research is in varying degrees also true for education and training albeit different capitalist formations have different histories. The Japanese and German private sectors invest more in education and training than do the Americans and Canadians. This does not change the basic role of the state with respect to research and training. Profit maximising firms prefer to train those already educated. As with research and development the state, unlike the private sector, does not have to concern itself with losing an investment in training an employee (human capital) who moves to another firm.

The disadvantage of an unalduterated neoliberal strategy is that it can inhibit the production of basic research and the critical mass of workers with the vital skills required to ameliorate the accumulation crisis. Who then is going to do the inventing, problem solving and symbolic analysis for the system? The corporate world is not becoming a simpler place; nor is its rate of change slowing. These examples of the essential role of the capitalist state with respect to capital accumulation are just that examples. Similar cases could be made for the states role in public health, the environment and legitimation crises.

We have argued that the context for so-called globalization is that capitalism entered into an economic crisis phase in the late 1960s. Crisis in this context does not mean catastrophic economic breakdown nor does it mean capitalism as usual (since 1945). In this conjuncture normal economic activity is not sufficient to restore prosperity because as accumulation slackens, less profit is available for the maintenance of those institutions whose relative stability and reproducibility permit the repeated fulfillment of an important socio-economic function.

Governments responding to the requisites of putative globalization cut corporate taxes and regulations lowering the costs of production in order to make their firms competitive in the more internationalized economy, which they helped to create with free trade agreements. Slow growth along with tax cuts meant these same governments decided to cut deficits and debt by shrinking the welfare state in order to prevent capital flight and to attract new capital to locales where corporation did not have to compete as much with the state for finance, labour or resources. Fighting inflation meant high real interest rates, increasing unemployment. The increasing reserve army of the unemployed lowered wage expectations and enabled capital to intensify the labour process and extend the working day. Some of the increased surplus from production was used for a spate of investment in new productivity enhancing machinery. The effects of less regulation, lower unit labour costs and less corporate taxes, all “required” by the new global economic context, had the effect of lowering the costs of production and enhancing productivity, particularly in the United States, requiring other nations to follow suite in order to be competitive. The various free trade agreements and the evolving GATS are intended to further reduce the states sovereignty over resources and regulations and to facilitate entry of capital into new arenas heretofore not as available for capital accumulation. Public education, public energy, the public water supply and public health care are all targets. The purpose of these initiatives is to raise the rate of profit and extend the domain of capital accumulation.

Interestingly, decades of neoliberal rule do not seem to have restored the golden hue to capitalism. The period between 1948-1973 exceeded the 1995-2000 period, even in the United States, in every respect-productivity, inflation, unemployment and profits except stock market valuation. This did not stop the system�s cheerleaders in the economics profession and mainstream media from ignoring this reality. As in the 1960s we began to hear the triumphant end to the business cycle. Even if the so-called decade long boom did occur in one country all that was needed was to emulate the neoliberal American model and all would prosper. Peruse the pages of Business Week or the Economist over the past few years and you can read the chorus in action. Other economic analysts have argued that the reason for the continued economic malaise is precisely the triumph of neoliberal policy where its faith in the long-run virtues of the free market are contradicted by the short-run and myopic investment practices of competing capitalists. The fact that that the state has been instrumental in dealing with market failure with respect to the requisites of capital accumulation highlights the continued critical role of the state and possibly increasingly regional industrial strategy. Education, basic research and infrastructure have never been an effective domain of competing for-profit enterprise. Indeed the state is likely to provide capital with cheaper health care, energy, and human capital, and is uniquely positioned to engage in the kind of scientific inquiry necessary to produce commodities in the future.

Multinationals and their national governments have attempted to free themselves from constraints with respect to regulations, labour, and taxes. Old institutions are contracted and/or transformed while new ones are formed as the system struggles to restore accumulation. The World Trade Organization and other free trade agreements can be seen as a strategy to use international rules to overcome domestic resistance to the multinationals interests. However, this attempt at turning the world into a free enterprise zone has led to legitimization problems for capital, as environmentalists, unions, and anti-poverty activists have coalesced to resist. They have largely abandoned parliamentary politics as the domain of capital and have declared their opposition in large numbers everywhere capital attempts to organize those rules with the noteworthy exceptions of meetings in police states. From Seattle to Quebec to Italy environmentalists, unions and citizen organizations demanding labour rights, environmental controls and public not private sovereignty over everything from health and education to energy and water supply.

The current ongoing world economic stagnation and September 11 may have undermined the neoliberal faith in the market and brought the state back into the management of the economy as governments promise subsidies to the ailing sectors, use fiscal stimulus and revert to military Keynesianism to mitigate the effect of economic and political crises. Five years or so of relative American economic success and decades of neoliberalism appears to have done little to restore global capital accumulation and for the first time in decades have raised the spectre of a legitimation crisis.

Bank for International Settlements,1998. 68th Annual Report. Bank of International Settlements, Basle, Switzerland.

Borosage, R., 1999. ‘The Battle in Seattle’, The Nation, December, 6.

Boyer, R., 1996. ‘The convergence hypothesis revisited: globalization but still the century of nations?’ in S. Berger and R. Dore (ed.), National Diversity and Global Capitalism, Cornell University Press, Ithaca, N.Y.: 29-59.

Brandt Commission, 1980. North-South: A Programme for Survival, Pan Book, London.

Brenner, R., 1998. ‘Uneven development and the long downturn: The advanced capitalist economies from boom to stagnation, 1951-1998’, New Left Review, 229: 1-265.

Chang, Ha-joon, 1998. ‘Globalization, transnational corporations, and economic development: can the developing countries pursue strategic industrial policy in a globalizing world economy?’ in D. Baker, G. Epstein, and R. Pollin (eds.), Globalization and Progressive Economic Policy, Cambridge University Press, Cambridge: 97-113.

Cherry, R., et al. (eds.), 1987. The Imperiled Economy, Book 1, The Union for Radical Political Economics, New York.

Cooper, I. and Kaplanis, E., 1994. ‘Home bias in equity portfolio, inflation hedging, and international capital market equilibrium’, Review of Financial Studies, 7(1): 45-60.

Dunning, J., 1997. ‘The advent of alliance capitalism’, in J. Dunning and K. Hamdani (eds.), The New Globalism and Developing Countries, United Nations University Press, New York: 12-50.

Dymski, G. and Isenberg, D., 1998. ‘Housing finance in the age of globalization: from social housing to life-cycle risk’, in D. Baker, G. Epstein, and R. Pollin (eds.), Globalization and Progressive Economic Policy, Cambridge University Press, Cambridge: 163-94.

The Economist, 2000. ‘Globalisation and tax survey’, January 29th: 9.

The Economist, 1995. ‘The myth of the powerless state’, October 7:15-16.

Felix, D., 1998. ‘Asia and the crisis of financial globalization’, in D. Baker, G. Epstein, and R. Pollin (eds.), Globalization and Progressive Economic Policy, Cambridge University Press, Cambridge.

Gordon, D.M., 1980. ‘Stages of accumulation and long economic cycles’, in T. Hopkins and I. Wallerstein (eds.), Process of the world System, 9-45. Sage Publications, Beverly Hills, California: 9-45.

Hamdani, K., 1997. ‘Introduction’, in J. Dunning and K. Hamdani (eds.), The New Globalism and Developing Countries, United Nations University Press, New York.

Hirst, P. and Thompson, G., 1996. Globalization in Question: The International Economy and the Possibilities of Governance, Polity Press, Cambridge, UK.

Horsman, M. and Marshall, A., 1994. After the Nation State, Harper Collins, London.

International Monetary Fund, 1993. International Capital Markets, Part I, Exchange Rate Management and International Capital Flows, IMF, Washington, April.

Keynes, J. M., 1967. The General Theory of Employment, Interest and Money, Macmillan, London.

Left Business Observer, 1998. ‘The US boom’, 81: 3. Maddison, A., 1995. Monitoring the World Economy, 1820-1992, Development Centre of the Organization for Economic Co-operation and Development (OECD), Paris.

President’s Information Technology Advisory Committee, 1999. Information Technology Research: Investing in Our Future, Executive Office of the President of the United States, Washington, D.C.

Obstfeld, M., 1998. ‘The global capital market: Benefactor or menace?’ Journal of Economic Perspective, 12 (4): 9-30.

Ohmae, K., 1990. The Borderless World, Collins, New York.

Organisation for Economic Co-operation and Development (OECD), 1998. OECD Economic Outlook. OECD, Paris, June.

Reich, R., 1992. The Work of Nations, Vintage, New York.

Sarel, M., 1996. ‘Nonlinear effects of inflation on economic growth’, IMF Staff Papers, 43(1):199-215.

Shrybman, S., 1999. The World Trade Organization: A Citizen=s Guide. James Lorimer & Company Ltd., Toronto.

Thurow, L., 1999. ‘Building Wealth’, The Atlantic Monthly, June: 57-69.

Thurow, L., 1996. The Future of Capitalism, New York, Penguin Books.

Tyson, L., 1991. ‘They are not us: Why American ownership still matters’, The American Prospect, Winter: 37-49.

United Nations, 1988. Transnational Corporation in World Development: Trends and Prospects, United Nation, Centre on Transnational Corporations, New York.

United Nations, 1992. World Investment Report 1992: Transnational Corporations as Engines of Growth. United Nations, New York.

United Nations, 1998. World Investment Report 1998: Trends and Determinants, United Nations, New York.

Weiss, L., 1997. ‘Globalization and the Myth of the Powerless State’, New Left Review, no. 225: 3-27.

Weiss, L., 1999. ‘Managed Openness: Beyond Neoliberal Global’, New Left Review, no.225: 126-40.

Wade, R., 1996. ‘Globalization and its limits: reports of the death of the national economy are greatly exaggerated’, in S. Berger and R. Dore (eds.), National Diversity and Global Capitalism, Cornell University Press, Ithaca, N.Y: 60-88.

Copyright remains exclusively with the author.